1. Assess your debt

2. Calculate your debt-to-income (DTI) ratio

3. Pick an approach to pay off debt

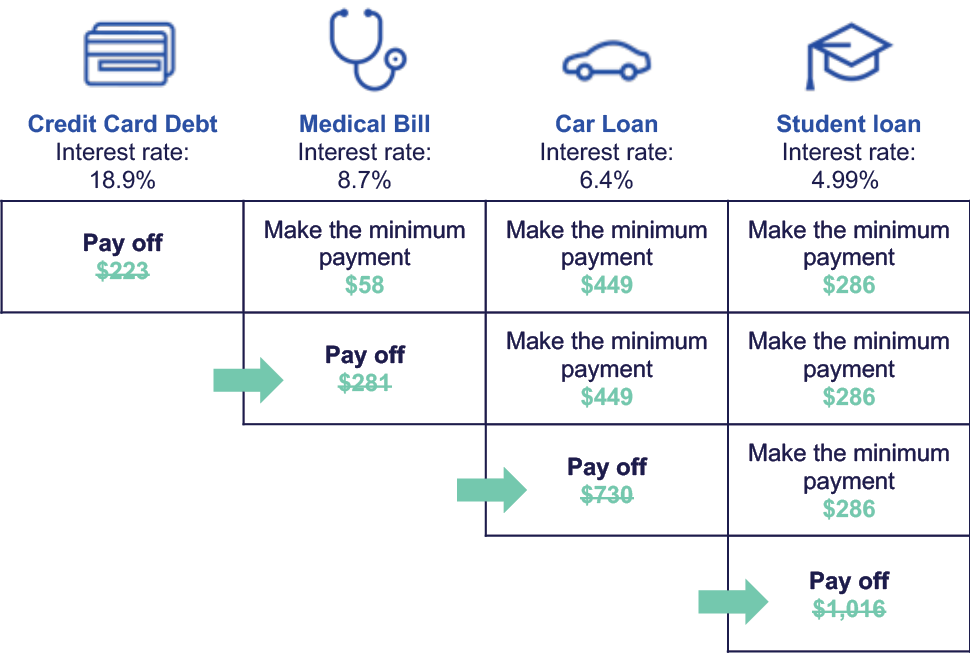

Debt avalanche

The debt avalanche method

Step 1: List your debts from highest to lowest interest rates.

Step 2: Pay extra on the debt with the highest interest rate but the minimum on everything else.

Step 3: When that debt is paid off, apply that payment to the debt with the next-highest interest rate.

Step 4: Repeat until all debt is paid.

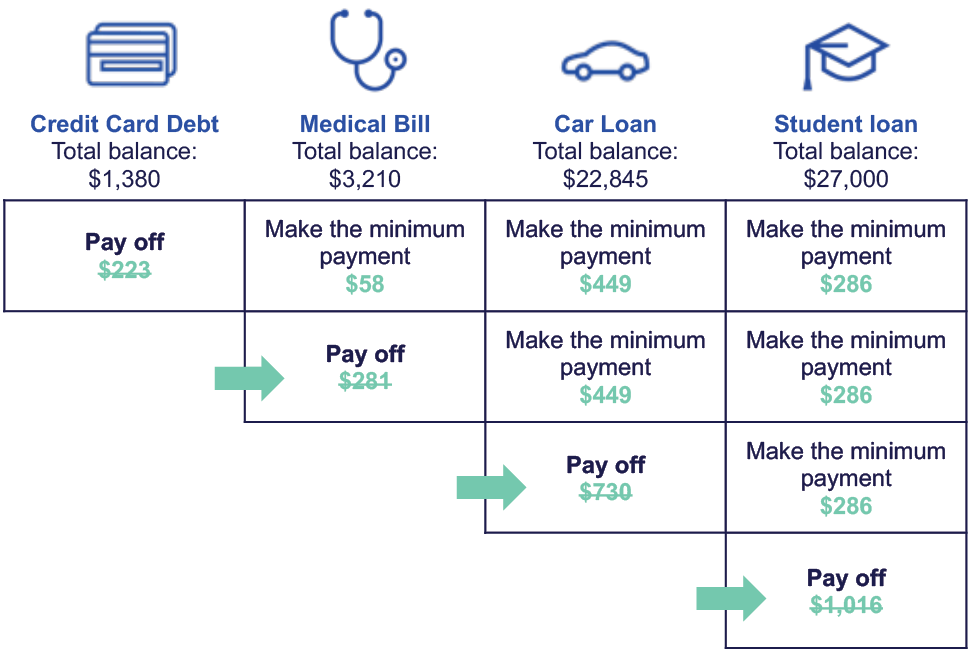

Debt snowball

The debt snowball method

Step 1: List your debts from the lowest balance to the highest.

Step 2: Pay extra toward your smallest debt but the minimum on everything else.

Step 3: When that debt is paid off, apply that payment to the next-smallest debt.

Step 4: Repeat until all debt is paid.

Wondering if you can save for other goals like retirement while paying down debt?

Check out our article “How do I pay off debt and save at the same time?”