1. Start (and stick to) a budgeting habit.

2. Be strategic with Social Security

3. Plan for Required Minimum Distributions

While the IRS allows you to put off paying taxes on certain tax-deferred retirement savings, eventually the government wants to collect its share. When you reach a certain age, they require you to take mandatory withdrawals each year called required minimum distributions (RMDs). You have to take RMDs from traditional accounts such as 401(k)s, 403(b)s, 457(b)s and IRAs – but not from Roth accounts during your lifetime if you’re the original accountholder.

It’s important to take these because if you don’t begin withdrawing until after your RMD age (see “RMD ages” chart), or if you don’t withdraw enough, you could be liable for a significant tax penalty on what you should have withdrawn plus ordinary income taxes on the full amount. If you don’t need the income when the time comes, consider working with a financial professional to review options for it that could benefit you in other ways, such as minimizing taxes.

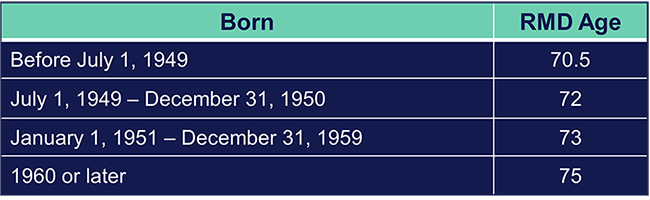

RMD ages

You must take your first RMD by April 1 of the year after the year in which you reach your RMD age. Then future RMDs have to be taken by December 31 each year. Keep in mind that if you delay your first RMD until the next year, you’ll need to take two RMDs that year, which could push you into a higher tax bracket.

If you’re still working and contributing to your employer’s retirement plan when you reach the RMD deadline, your adjusted RMD beginning date for that account is April 1 of the year after you terminate employment there.

How do you know how much to withdraw? Your RMD for each account is based on 2 things: Your account balance at the end of the year before and a life expectancy factor that corresponds to your age. To calculate the amount, divide the amount of your balance on Dec. 31st of the year prior by your life expectancy factor as published in IRS Publication 590-B. As long as you have money invested in your current retirement plan, we’ll automatically calculate your RMD and distribute the proper amount to you each year.

4. Understand the impact of taxes.

Federal taxes on retirement income